Apple Pay ist endlich da; offensichtlich sehr zufriedene erste Bankpartner; Apple erweitert NFC-Ökosystem; erste vielversprechende Kundenreaktionen

Nun ist es also soweit. Sechs iPhone-Generationen (6, 6s, SE, 7, 8, X-Reihe) wurden zwischenzeitlich vorgestellt, bis es zum angekündigten Apple Pay Launch in Deutschland kam. Deutschland kommt sehr spät ins Spiel: 26 Länder waren vor uns live. Dafür hat Apple gestern in München in der Allianz-Arena aber deutlich mehr gezeigt, als ausschließlich das mobile Bezahlen am POS. Ausgewählten Impulsgebern (darunter wir von Paymentandbanking.com) und Pressevertretern von Tech- Nachrichten bis Lifestyle-Medien wurde von Apple eine ganze Bandbreite vorgestellt: Die Allianz-Arena ist eines von zehn Stadien weltweit, in denen Apple durchgängig ein mobiles Ticketing implementiert hat. Der Fan kann lediglich mit seinem NFC-Telefon oder Smartwatch und dem Ticket in der Apple Wallet ins Stadion und dann auf seinen Sitzplatz. Zusammen mit dem Apple Pay Launch, wurde dies erstmals überhaupt der Öffentlichkeit präsentiert. Im Stadion wurden ferner alle Kassenplätze, von der Wurst übers Bier bis zum Merchandisingshop, mit NFC-Terminals und Kartenakzeptanz ausgestattet.

Auch wenn Apple sich viel Zeit für den Start in Deutschland gelassen hat, schien der Launch in Deutschland eine hohe Priorität zu haben und wurde, ganz Apple-like, perfekt durchorchestriert. Karlheinz Rummenigge machte öffentlichwirksam eine erste Apple Pay-Transaktion und Apple hat die internationalen Apple Pay Executives eingeflogen. Darunter viele ehemalige Mitarbeiter von PayPal, Visa, MasterCard, die das Payment-Geschäft in allen Details beherrschen.

In einer Demo-Area zeigte Apple ferner die sehr gelungene und bequeme mobile In-App-Zahlung mit Apple Pay am Beispiel des Münchner Mobilitäts-StartUp Flixbus. Auch klassisches Onlineshopping mit Apple Pay an einem Mac und iPad fehlte nicht. In allen drei Beispielen des mobile/online-Payments erkennt das Gerät automatisiert die Apple Pay Unterstützung der Akzeptanzstelle und blendet das schlanke Bezahlfenster ein, bevor dem Kunden überhaupt eine Zahlseite mit anderen Zahlmethoden dargestellt wird. Eingabe von Zahlungsdaten, Versandadressen oder gar starke Authentifikationen, die oft nicht vom Kunden gedacht sind, entfallen gänzlich. Der Kunde bezahlt mit Touch-ID am Rechner, iPhone und iPad und bei neueren mobilen Devices mit Face-ID. Der Handel wird die deutlich höhere Conversion lieben und die PayPals, Klarnas, Lastschriftverfahren, Online-Überweisungen dieser Welt werden bei einer stärkeren Kundennutzung ein massives Problem mit dem “Share of Checkout” der Apple-User bekommen. PayPal konnte über genau diesen Weg mittels Express-Checkout ihren Marktanteil im Online-Zahlungsmix in wenigen Jahren fast explosionsartig steigern. Sie boten weniger Abbrüche für den Handel und mehr Bequemlichkeit für den Kunden. Dieses Erlebnis toppt Apple für seine User, die, laut eigenen Aussagen, einen Marktanteil von 29% in Deutschland ausmachen.

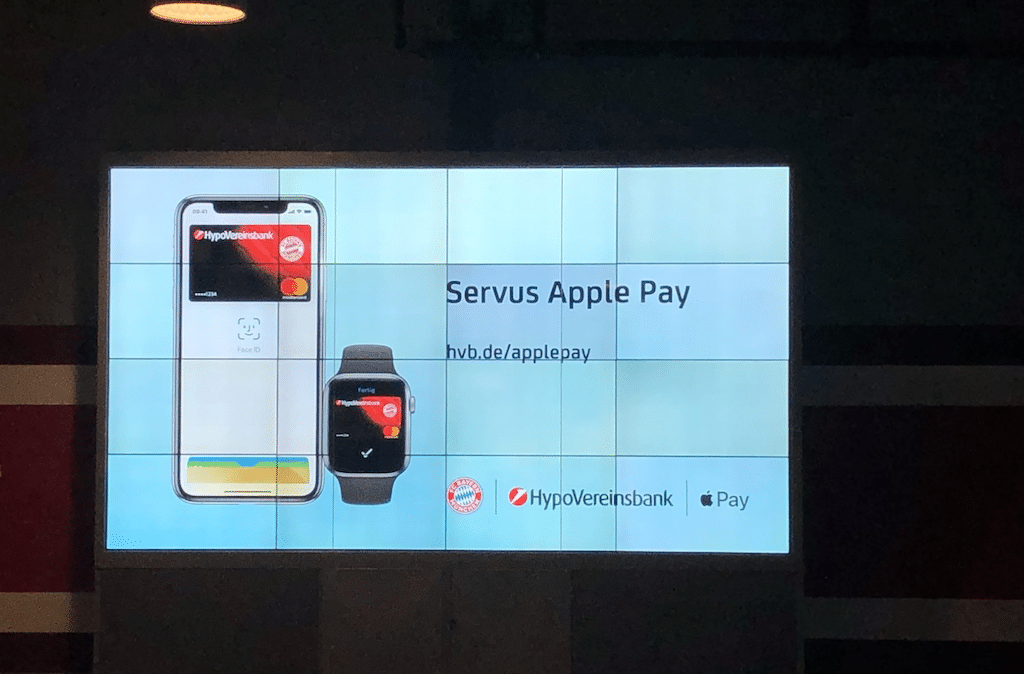

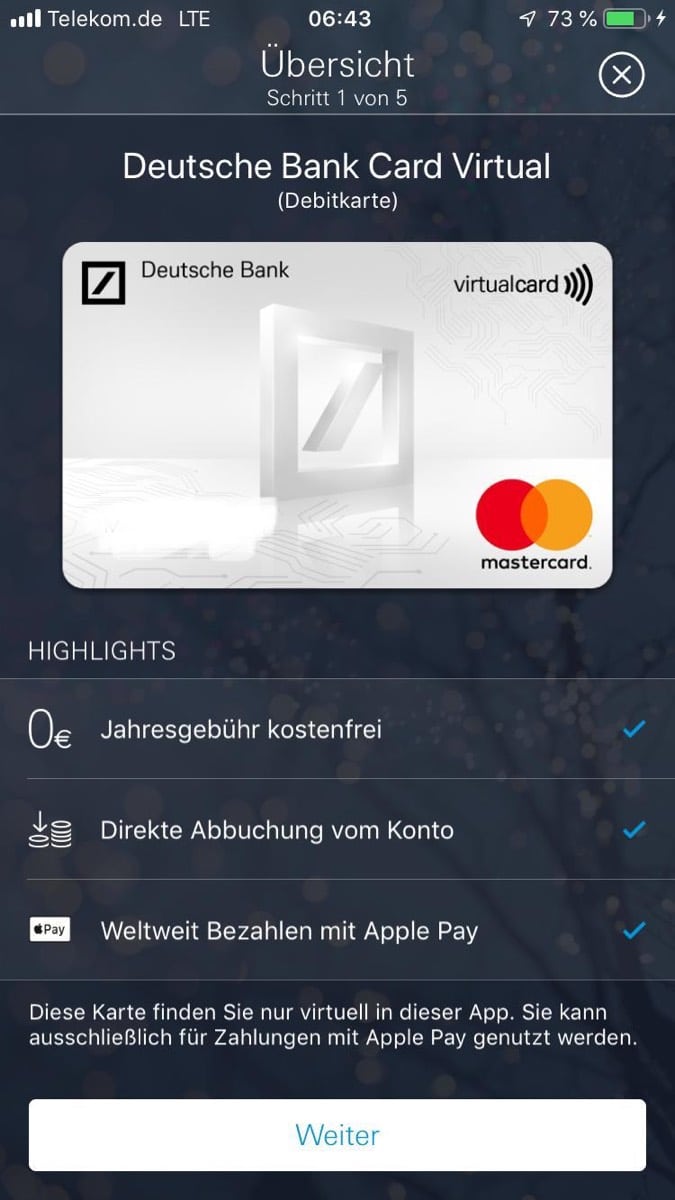

Während die teilnehmenden Banken seit Wochen bekannt waren, hat Apple vor Ort drei ausgewählte Bankpartner präsentiert. Die Deutsche Bank hatte mit MasterCard eine Loge, die Comdirect zusammen mit VISA und natürlich die HVB als Anbieter der lokalen FC-Bayern Co-Brand Karte. Die Deutsche Bank präsentierte vor Ort erstmals ihre neue virtuelle MasterCard Debit Karte. Der Kunde kann diese Karte, die dauerhaft von der Jahresgebühr befreit ist, direkt aus der Banking-App heraus beantragen. Die Karte autorisiert, wie eine x-beliebige Girocard, direkt gegen das Bankkonto. Der Kartenregistrierungs- und Aktivierungs-Prozess für Apple Pay aus der Banking-App der Deutschen Bank ist aus meiner Sicht “Best-in-Class” gelungen. Meine anderen beiden Karten konnte ich jeweils nicht mit der jeweiligen App aktivieren, sondern “nur” über die Apple-Wallet. Es gab danach noch Friktionen mit der AppleWatch, verbunden mit einer getrennten Aktivierung der Karten, ausschließlich dafür. Der von der Deutschen Bank gewählte Weg über die App hätte das vermieden. Chapeau, da ist die Deutsche Bank mit ihren Prozessen und ihrer UX wirklich auf einem Niveau mit den jungen Challengerbanken wie N26 und Co. Das ist alles andere als selbstverständlich, schaut man sich die anderen strauchelnden Digitalprojekte der deutschen Banken und Sparkassen an.

Michael Koch, verantwortlich für Online- und Mobilebanking der Deutschen Bank, sprach bezüglich der MasterCard Debit-Karte und Apple Pay als dem stärksten Produktlaunch der Deutschen Bank überhaupt. Wesentliche KPIs hätten die Erwartungen weit übertroffen. So konnte die Deutsche Bank gestern Vormittag hohe dreistellige Kartenanträge pro Minute verzeichnen und die Besuche der Deutschen Bank Homepage waren sechsfach höher als sonst. Dieser Kundenansturm ist sehr beeindruckend. Ich denke das Institut wird so alleine über 50.000 neue Karten am gestrigen Tag abgesetzt bzw. aktiviert haben. Auch ein Comdirect Mitarbeiter schrieb bei Twitter von einem selbstgesetzten Tagesziel von 10.000 Registrierungen (Tweet leider nicht mehr auffindbar) und die im Vergleich eher kleine Hanseatic Bank berichtete auch von 1.200 Registrierungen in den ersten Stunden. Für den gesättigten deutschen Kartenmarkt sind dies schier unglaubliche Zahlen, die vermutlich von den nationalen Konkurrenten mit großem Neid betrachtet werden.

Kommen wir zu dem was fehlte?

1. Namhafte große Banken boykottieren weiter

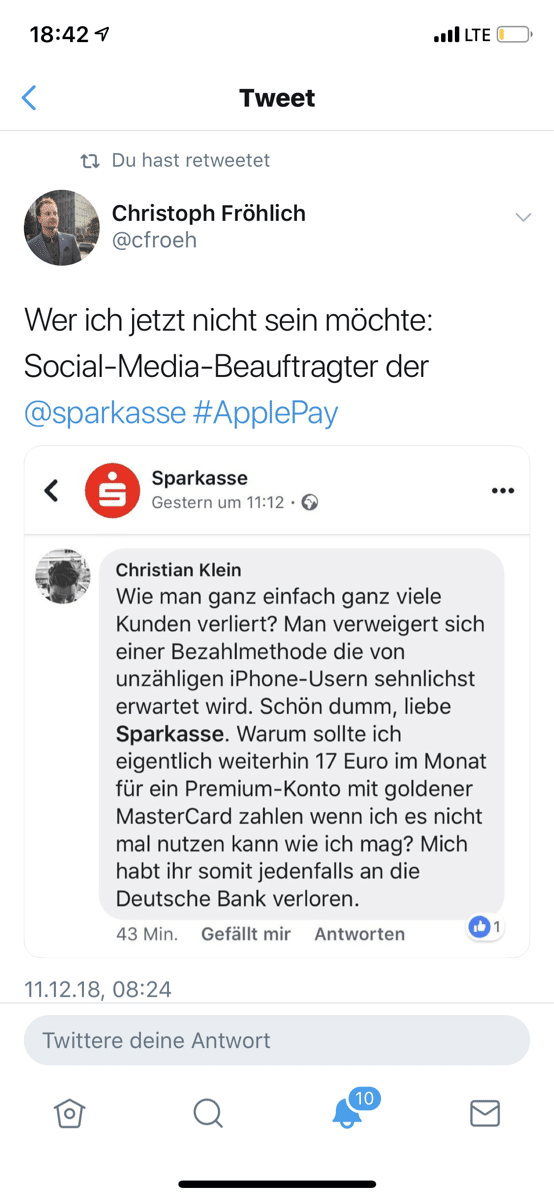

Zeitgleich zum Start von Apple Pay haben andere Banken ihre Teilnahme als “coming soon in 2019” angekündigt, darunter die DKB, ING, Consors, Revolut. Es geht aber ein Riß durch die deutsche Kreditwirtschaft: Als große namhafte Kreditinstitute fehlen weiter die Commerzbank, die Postbank und vor allem die Sparkassen und VR-Banken. In meiner Twitter-Filterblase las ich von vielen Kunden, die sich bei den Social Media-Teams von Banken über ihre Nicht-Teilnahme beschwerten. Auch wenn der eine oder andere Banker solche Kunden als (O-Ton) “Apple-Fanboys” verunglimpft, sollte doch das Beispiel Barclaycard in UK eine Lehre sein. Ein Applemanager wies grinsend darauf hin, daß Barclays sich anfangs mit Händen und Füßen gegen Apple Pay wehrte. Fehlende Kundentraktion auf den eigenen Alternativprodukten und abwandernde Kunden im hart umkämpften Kartenmarkt UK haben schließlich zu einem Einlenken geführt. Auch betonte der Manager, daß die Firstmover-Banken in UK bis heute “top-of-wallet” bei den Kunden sind und somit deutlich höhere Transaktionen und Umsätze auf den Karten verzeichnen. Wenn es bei uns auch so kommt, bedeutet das gute Nachrichten für die Deutsche Bank, Comdirect und Co. Der deutsche Sparkassenverband fühlte sich gestern sogar zu einer Pressemitteilung gezwungen und forderte einmal mehr die Öffnung der NFC-Schnittstelle durch Apple. Auch hier hilft der Blick ins Ausland: Mit ähnlichen Strategien sind Banken in Australien sogar gerichtlich gescheitert. Sollte einmal mehr die Politik wichtiger sein als der Kundenwunsch und auf Zeit gespielt werden? Der Erfolg bei Kunde und Handel von PayPal, Google und jetzt Apple im digitalen Zahlungsverkehr liegt schließlich originär darin begründet, daß der Kundenbedarf über Jahrzehnte von den Paymentverantwortlichen deutscher Banken und Sparkassen komplett ignoriert wurde. So positionieren sich die Sparkassen als die aktuell besten pro-bono Vermarkter der Lösungen von Amex, Boon, Comdirect, Deutsche Bank, Hanseatic, N26 und VIMpay. Denn die Nachricht an ihre Kunden, die an Apple Pay interessiert sind, ist eindeutig: Es gibt bis auf weiteres kein Apple Pay bei uns. Stattdessen fordern wir (als kleine regionale Sparkassen von einem der größten Unternehmen der Welt) etwas, woran weltweit bisher alle Banken gescheitert sind: Öffnung einer proprietären API und Schnittstelle. Im Umkehrschluß bedeutet das: Der Kunde muß entweder warten bis Apple sich bewegt (sehr unwahrscheinlich) oder die Sparkassen sich auf EU-Ebene in einem mehrjährigen Kartellverfahren eventuell durchsetzen (eventuell möglich). Wenn zwei sich streiten freut sich ein Dritter und die möglichen Dritten sind die Fistmover bei Apple Pay.

2. Girocard spielt keine Rolle

Die großen Banken haben ihre traditionellen Konto-Debitkarten (Girocard, Maestro, VPay) nicht in den Launch integriert. In der Pressekonferenz begründeten z.B. die Vertreter der Deutschen Bank und MasterCard dies mit der weitaus größeren internationalen und vor allem Online-Akzeptanz im Vergleich zur klassischen Girocard. Eine so klare Positionierung gegen die Girocard habe ich aus dem Mund eines führenden deutschen Kreditinstituts noch nicht gehört.

3. Apple Pay Cash

Das USA eingeführte Person-to-Person Zahlverfahren Apple Pay Cash wird in Deutschland bislang nicht angeboten. Wenn ich spekulieren darf, ist die Apple Pay Abdeckung bei den Kunden einfach noch nicht groß genug in Deutschland. Meines Erachtens wird dies von Apple erst dann eingeführt, wenn die Banken- und Kundenabdeckung größer wird.

4. Abwertende Aussagen zur NFC-Akzeptanz im Handel

Lange war die fehlende NFC-Akzeptanz im Handel ein Problem in Deutschland. Dies spielte gestern keine Rolle mehr. Wie selbstverständlich wurde schon von der “annähernd flächendeckenden Akzeptanz” gesprochen. Auch online, nicht zuletzt zu sehen am Beispiel Flixbus, bieten namhafte (internationale) Händler und Plattformen längst eine breite Akzeptanz für den Kunden. Händler und Handelsketten, die sämtliche relevanten Bereiche des täglichen Lebens abdecken, haben in den letzten Monaten und Jahren ihre Hausaufgaben gemacht und ihre Onlineshops bzw. POS-Terminals auf die kontaktlose Akzeptanz umgestellt.

Fazit

Alles in allem war es ein sehr gelungener Marktstart von Apple Pay in Deutschland. Jetzt ist es an Apple und den ersten Banken die Nutzung der Kunden zu stimulieren. Wir dürfen noch einige Marketingkampagnen im TV sowie Online- und Printmedien erwarten. So hat sich die Deutsche Bank den Sound einer erfolgreichen Apple Pay-Zahlung “Ba Bing” als Wortmarke schützen lassen und nutzt diesen in ihrer Apple Pay Marketingkampagne. Mit dem Erfolg in der Nutzung, als auch den jetzt bereits beeindruckend sichtbaren Erfolgen bei Neukunden und Aktivierung von Bestandskunden, werden die noch zögernden Banken sicherlich bald nachziehen. So “different is Germany” dann auch nicht. Warum soll es bei uns anders sein als in anderen Ländern?