Das Thema “Mobility”, im speziellen die eScooter, waren als “paymentverwandtes” Thema schon öfters Inhalt unserer Diskussionen. Kommend von der Theorie nun die Praxis: knallharte Realität in Form eines Wochenendtrips nach Kopenhagen. Zwei Erwachsene, drei Kids (5,11,14) brauchen Mobilität beim Erkunden der Stadt.

Kopenhagen scheint hier weit vorne, will sich wohl auch als “modern” und “urban” positionieren. Fast liberal (aber auch etwas “grotesk” hat man mich vor ca. 1-2 Jahren mit Schimpf und Schande und einem Uber aus der Stadt gejagt). Anyway, so ein Uber Jump wäre schon als Alternative zum Scooter interessant gewesen. Weiter eBike Share Dienste jedoch Fehlanzeige. Einzig verbliebener Bike Share Dienst, der Donkey – die Dinger schauen aber inzwischen so aus, wie sie heißen und werden schon als Ersatzteilversorgung benutzt… Ein Dauermodell?

Die Verfügbarkeit:

An allen Ecken und Enden steht so ein Ding rum, die “Leihfahrräder” sind ja alle wieder verschwunden, so schnell sie der Chinese aus der alten Antonow über den europäischen Großstädten abgeworfen hat, so schnell scheinen sie auch wieder verschwunden zu sein. Ich hoffe die eScooter Jungs ziehen Ihre Lehren daraus. Trotzdem frage ich mich, warum das Thema “Fahrrad” schon wieder “durch” zu sein scheint?

Viele der Strecken, die man mit dem Scooter macht, sind ohne Probleme fahrradtauglich. Zumal die Fahrräder auch günstiger in der Anschaffung und Wartung sein dürften. Der Wunsch der Scooter Companies einen medienträchtigen Effekt zu erzielen (wir ersetzen das Auto) muß erstmal nachgewiesen werden. Von uns gesprochen, wir hätten da eher einiges zu Fuß gemacht und den ÖPNV genutzt. Vielleicht hätten wir weniger gesehen von der Stadt…Fürs “Pendeln” sind die Dinger noch zu teuer und am Ende fehlt dann doch genau ein Roller, wenn man ihn braucht.

Fazit ist aber

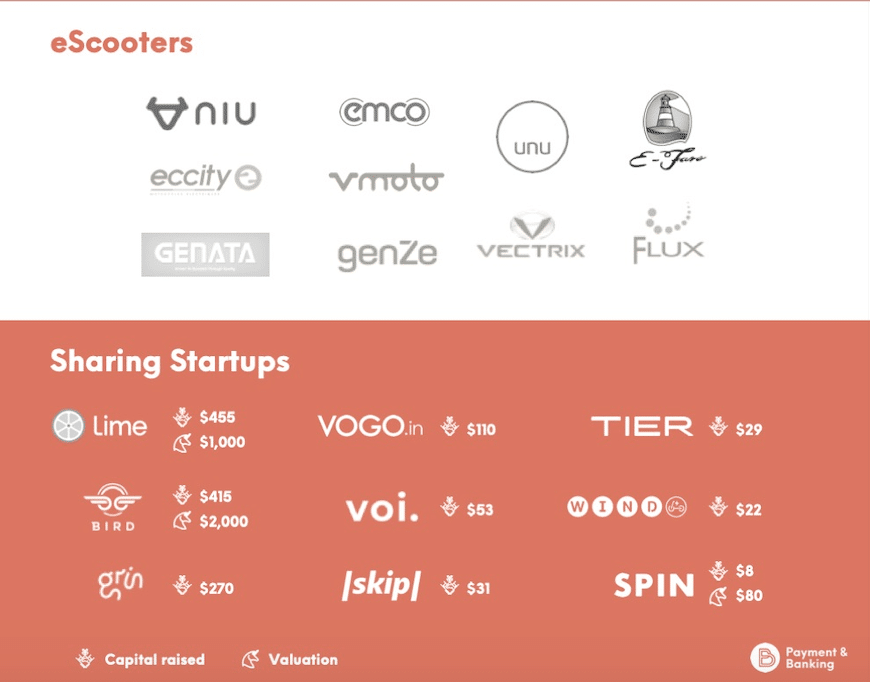

- Man braucht sofort mehrere Apps – in Kopenhagen Voi, Lime & Tier

- Am Abend wird es eng mit der Fortbewegung. Angeblich werden die Dinger ab 21.00 Uhr alle wieder eingesammelt (ob sich das lohnt?)

Der Roller

Irgendwie alle gleich auf den ersten Blick. Vermeintlich alle vom selben “Chinesen” produziert und ausgeliefert. Im Detail ist das “Tier” etwas schöner und der “Lime” etwas klobig (was dazu führt, dass schon der ein oder andere Randstein beim Anheben schön in die Bandscheibe ging). Es gibt zwei grundsätzliche Modelle, die sich v.a. bei der Bremse unterscheiden. Handbremse (wie beim Fahrrad) oder elektronische Bremse in Kombi mit Hinterradfussbremse. Letzeres scheint das neuere Modell zu sein. Es dürfte interessant werden, ob bei neueren Generationen noch etwas in der Pipeline ist?

Was ich vermisst habe: Eine Möglichkeit das Handy anzubringen, denn Navigation ist auch hier nötig. Und der Fahrkomfort bei Kopfsteinpflaster, denn dabei ist mir gefühlt drei Mal fast das iPhone aus der Hand gefallen. Die GPS Funktion ist noch zu ungenau oder die Technologie an sich. Mindestens drei Mal war der Roller nicht auffindbar oder wir alle blind.

Führte dazu, dass man nicht mehr nach “App” sucht, sondern einfach durch die Straße läuft und hofft einen zu finden. Wo der “Hund hier begraben” ist, erschließt sich nicht, interessiert den Kunden aber auch nicht.

Interessanterweise scheint Lime etwas stärker darauf zu achten, dass die Fahrer 18 sind. Bei Voi & Tier fehlt der Hinweis. Wie relevant die Altersgrenze ist, mag ich nicht sagen. Wir haben auf jeden Fall für die beiden Kids (11,14) jeweils zwei Accounts registriert. Mit “Papas CC” ging das ohne Probleme. Erstmal – alles weitere siehe unten.

Ein interessanter Wert – Höchstgeschwindigkeit

a) Lime – 19,1 kmh

b) Voi – 20,1 km/h

c) Tier – 20,7 km/h – macht dem Namen alle Ehre

Tests waren alle mit dem gleichen Lebendgewicht. Keine Schummelei. Gefühlt reichen die 20 km/h aus um entspannt durch die Stadt zu kommen. Das Rennen mit den Radlern ist auf Augenhöhe (für die Masse). Und man fühlt sich auch ohne Helm noch “irgendwie sicher”.

Die App

“Alles eine Suppe” – Voi und Tier unterscheiden sich eigentlich gar nicht. Einziges nettes Feature (bei allen) ist es ein Bild des Abstellortes zu machen, damit ihn der Nachfolger einfacher findet. Sharenow – Hallo?

Lime ist etwas mehr “ausgereifter, man hat den Eindruck, dass man hier schon 1-2 Releases weiter ist. (z.B. Notifications, Rechnung per eMail, echte Wallet Funktion) etc. Tier ist “sehr basic” – hatte schon das Gefühl mir werden nicht alle Funktionen freigeschalten. Es gibt aber wohl nicht mehr. Voi ist “in between” – eine einfache Mischung ohne dabei speziell zu sein oder hervorzustechen. Auffällig war hier, dass relativ viele Roller dann nicht buchbar waren und dies leider erst am Ende der User Journey erfährt. Warum nicht sofort?

Allen ist gemein, dass es “Mobile Only” ist. Auch da bin ich mir nicht sicher, ob das nicht am Kunden vorbei gedacht ist. Einige Funktionalitäten (z.B. Userprofile, Payment Methoden etc.) sind über das Web durchaus sinnvoll. Nicht alles will ich machen, wenn ich direkt vorm Roller stehe.

„‚Mobile Only‘ könnte am Kunden vorbeigedacht sein.“

Der Buchungsprozess

Eigentlich Easy: mit dem “GPS Tracking Feature als möglicher Differentiator beim Tier, wenn da nicht das Payment wäre… siehe unten

Die Brands

Sind eigentlich total egal – für mich ein Business dass nach Konsolidierung schreit. Einzig der Brandname “Tier” hat etwas “humoristisches”, wenn die Kids durch die Stadtlaufen und fragen/schreien – “da drüben stehen ein paar Tiere” – funktioniert aber auch nur in deutsch.

Und nun zum Kernthema, dem Payment. Wie oft haben wir postuliert, das Payment verschwindet, es wird zu Commodity, zur Infrastruktur. Der Nutzer will nutzen – nicht zahlen. So weit so gut, die eScooter als relativ neue “Industrie” bieten noch einmal einen Praxistest. Was fällt auf:

a) Zahlmethoden – nur einer (Lime) – bietet Apple Pay an (Google Pay konnte mangels Gerät nicht überprüft werden), Tier und Void begnügen sich mit der guten alten Kreditkarte. Von PayPal nichts zu sehen (fehlende “echte” CardOnFile/Recurring Funktionalität) von lokalen Zahlarten ganz zu schweigen (“War nicht ein mir bekanntes Zitat aus der eCommerce Welt “Ohne Dankort brauchst du in Dänemark gar nicht anfangen”). Fairerweise kann es ja sein, dass man “uns” als Deutsche erkannt hat, die natürlich keine Dankort haben. Ich zweifle etwas daran, dass es nach dieser Logik funktionierte. Auch den Chinesen sucht man vergeblich und es wird spannend, wenn der sich mal traut alleine zu reisen. Auf den DE Launch und das Portfolio bin ich gespannt.

b) Das Registrieren der Zahlmittel: Alles Easy – ging schnell und unkompliziert, sei es Apple Pay oder normale CC (Test war mit Mastercard) hier gab es keinen Unterschied im Prozess bei Lime, Voi und Tier. Lime bietet eine Art “Wallet Funktion” mit Top Up an also kein direktes durchbuchen auf das Zahlmittel. Für den Endkunden kein direkter Vorteil, für Lime ggf. schon. (Kosten/technologisch einfacher integrierbar etc.)

c) Das Nutzen der Zahlmittel: Bei der ersten Fahrt lief alles wie geschnitten Brot. Nach weniger als 20 min waren 4 Accounts bei jeweils drei Anbietern und jeweils einem Zahlmittel (meine CC) up and running. Und wir auf den Dingern unterwegs zum Frühstück.

Soweit so gut – dann beginnt der Spaß…

a) Am Ende des Tages ging keine Buchung mehr durch, die Issuing Bank hat alle Transaktionen declined – (DKB) – hier ein klarer Appel von mir an die unterschiedlichen Stakeholder

- An den Issuer: Wenn ihr aus Fraudgründen declined, lasst es bitte den Endkunden wissen, denn ihr wollt ihn ja schützen und das in Realtime und nicht erst nach proaktivem Anruf des Kunden. Der Customer Support war gut, aber warum den Kunden hier als Trigger nutzen?

- An den eScooter Betreiber: Sprecht mit dem Issuer und monitored die declinerRates pro Bank und “pushed” hier denn es ist euer Geld!

- An den eScooter Betreiber: Arbeitet an der Usability und an Alternativen!

- An den Acquirer: Arbeitet sauber mit den MCC’s um die Risksysteme nicht zu verwirren. Ich habe die Buchungen sowohl als “Transport” als auch als “Software” oder als “allgemeine Dienstleistung” in meinem Account. Was soll ein halbwegs schlaues Risk/Fraudsystem damit anfangen?

- An den Issuer: Arbeitet an euren Risksystemen! Ich gebe zu, dass die Tatsache, dass die Karte in 4 Apps hinterlegt war, schon “komisch” war. Mit etwas Mühe hätte man das Muster aber erkennen können. Nutzt euren vorhandenen Kommunikationskanal zum Kunden. Warum kam da nie wenigstens eine SMS?

b) nach einem Telefonat mit der Bank war die Karte wieder freigeschalten. Interessanterweise wurde sie “beim Tier” weiter declined, vermutlich gibt es dort noch ein internes “Risksystem” denn einmal decline bedeutet erstmal länger declined.

c) “Rettung” war dann Boon in Kombi mit Apple Pay (Disclaimer – arbeite bei der Wirecard)! Zum Boon TopUp wurde dieselbe Karte verwendet :-) – führte dann in Konsequenz zu 24h Nutzung von Lime only – der Rest war ja leider geblockt.

Was sonst noch so war:

Nebeneffekt: Bei Lime wurde mein Account in CAD geführt, keine Ahnung wieso? Die Karte wurde auch in CAD gecharged. Hierzu ein paar Vermutungen:

a) ein geheimes DCC Geschäftsmodell

b) der eMoney Issuer von Lime ist Kanadier

c) Implementierungsfehler

d) Acquirer von Lime hat einen “falschen” Business Case aufgesetzt

Mehr ins Detail gehen konnte ich nicht, let’s see., meine Vermutung ist jedoch Lösung c), da auch auf der Rechnung Währungen wild durcheinander gewürfelt werden. Was für mich kein Thema ist, ist für den Joe Sixpack jedoch keine vertauensbildende Maßnahme. Das Durcheinander zwischen DKB, CAD und EUR hat auf jeden Fall dazu geführt, dass ich keine Ahnung mehr hab, was der Spaß überhaupt gekostet hat.

„Das Durcheinander zwischen DKB, CAD und EUR hat dazu geführt, dass ich keine Ahnung mehr hab, was der Spaß überhaupt gekostet hat.“

Conclusio:

Gerade in einem neuen Markt mit neuen Produkten die sich am Ende kaum unterscheiden (und wo man erst Vertrauen und USP aufbauen muss) ist die User Journey das A&O denn ist diese einmal verbockt ist diese schwer wiederzugewinnen. Und da genau spielt Payment rein, denn genau hier müsst ihr in die Tiefe gehen. Payment ist ein Kern eures Produktes und elementarer Teil der Wertschöpfung. Hier müsst ihr so schlau sein, wie eure Dienstleister, im Best Case noch schlauer. Schaut auf die Gaming und Gambling Industrie. Die Payment Manager dort sind in der Regel schlauer, als die Ansprechpartner der Dienstleister. Das mag traurig sein, am Ende ist jedoch das/euer Geschäft wichtiger als eine Diskussion darum wo welches KnowHow herkommt.

Die Roller an sich mag ich und ich hoffe auf ein anderes Schicksal als bei den Bikes und dass sich diese “irgendwann” in einer allumfassenden Mobilitätsvision widerspiegeln und nicht den “Call a Bike Tod” in einem Großkonzern sterben.