A contribution from Robin Brass

Wirecard has long been the most traded and hotly discussed share in Germany. Many people ask themselves whether Tesla does not also have many parallels with Wirecard.

All in all, the picture does indeed show some parallels, but also some major differences, which should certainly not only be of interest to investors.

The big short

Large short bets – i.e. speculation on falling prices – are made on both shares.

At Wirecard, some 30 million shares or 25 % of the free float were recently hoarded. In the meantime, this corresponded to a share value of over three billion euros. Owing to the sharp drop in share price from over €100 to €2 since mid-June, the shortsellers have meanwhile generated over three billion euros in profit.

At Tesla, the dimension is even greater due to the high market capitalization. Currently, 20 billion dollars, i.e. over 12 million Tesla shares are hoarded – which corresponds to a free float of almost 9%. This means that Tesla is the most shorted share in the USA in terms of volume. However, there is at least one major difference to the Wirecard share in this respect, as the shortsellers have so far got a bloody nose at Tesla and lost an incredible 22 billion dollars in 2020 alone. [figures from S3 Partners].

The polarizing CEO

Markus Braun but also Elon Musk always heated up the minds in the past. Both are seen as visionaries by some, as great charlatans by others. What unites them, however, is their common hatred of shortsellers. According to the Financial Times, Markus Braun liked to sue his critics and even had short sellers followed by detectives. With Musk, the whole thing is usually fought out rather verbally.

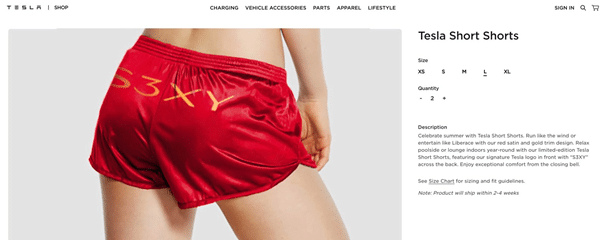

Just recently, for example, he had released a pair of short shorts (pants) for only $69,420. A wink with the fence post? The number behind the decimal point could also be a hint at the announced buyout of the Tesla stock in 2018 – at a price of $420 ! Funfact: Interestingly enough, this is also the abbreviation of marijuana lovers.

No profit?

Both companies argued that they were not making a profit. For years, Wirecard, with EBITDA margins of almost 30%, had been a mystery to the financial world: How could the company be so much more profitable than the competition? In the meantime, many signs indicate that the company had been virtually making no profit for years and that everything was fake.

At Tesla, there have been numerous quarters of heavy losses in the past, which meant that, at least until 2019, the question always had to be asked: How long will investors continue to pump money into the company to keep it alive? For four quarters now, Tesla has been generating smaller profits and the cash flow has also improved massively, which at least takes away the pressure of insolvency.

However, critics continue to mention that the profit was actually only made by selling climate certificates. Without these, Tesla would have had to continue to report a loss. In the last quarter Tesla announced a turnover of about 6 billion dollars including about 400 million dollars from CO2 certificates and a profit of about 100 million dollars.

Therefore, this statement contains a certain truth, but it is publicly known and, unlike Wirecard, not an invented number! Tesla is also on the verge of great growth, as the demand for electric cars is increasing and new factories will be opened soon. It is expected that this will also improve profitability.

Poor technology

At Wirecard, it was often argued that the scalability of the business model was not available as is the case with competitors such as Stripe or Adyen. In this case, the competition built a real platform with only one technology (gateway etc.). In the case of Wirecard, on the other hand, many entities with their own technology stacks were purchased and even within the European business no real platform could be demonstrated.

At Tesla, criticism was voiced due to the larger gap dimensions in the cars or delivery problems that the company would never be able to keep up with established competitors such as BMW or Audi because the necessary quality was not achieved. In the meantime Tesla has survived the “manufacturing hell” with the mass production of the Model 3s. However, the manufacturing quality still lags behind premium brands. However, Tesla is certainly 2-3 years ahead of most traditional manufacturers in the areas of software (over the air updates etc), self driving and especially with its battery technology.

Valuation

For both companies, the valuation or Valuation was always a reason to bet on falling prices.

In 2018, Wirecard achieved a market capitalization of 24 billion euros with sales revenues of around two billion euros, i.e. a valuation of 12x sales revenues. Tesla with 25 billion dollars in sales and a market capitalization of 280 billion dollars thus also has a valuation of 11x sales. Such high valuations are usually only paid for by excellent software companies such as Adobe, Atlassian or Nemetschek. At Wirecard, the business model was also based on software, but the high quality was certainly never available for such ratings. At Tesla, on the other hand, one should know that other car manufacturers tend to trade at 1x-1.5x sales.

The latter is currently probably the biggest argument of the short sellers that the valuation of the Tesla share is massively overvalued and one should therefore bet on falling prices. However, the current valuation of the stock should discount future cash flows and depending on expectations, one can calculate lower or even higher prices – but without doubt the stock is very highly valued.

“Probably the biggest argument of the short sellers at the moment: The Tesla stock is massively overvalued.”

Competition

In the past, Wirecard also had many competitors and incumbents. Large banks, technology companies, credit card companies, PSPs etc. Although the market grew relatively strongly and the change from cash to digital payment options is likely to continue for many years to come, one could already see price pressure in tenders, especially in Europe – especially for standard topics such as pure payment acceptance. Overall, however, this topic is likely to play a much greater role for Tesla, as the car manufacturer is pushing into an established market that has long been dominated by many competitors with “deep pockets”. This thesis is supported by the fact that no newcomers to the car market had survived since the Second World War – until Tesla came along.

However, Tesla has already been certified to end in 2016 and 2017. tesla killers like Rivian, Byton, Faraday Future, Dyson etc. wanted to conquer the market. Nothing has come of it so far, because some of the new competitors have long since gone bankrupt and others are still struggling to get their first car on the road. In addition, the traditional OEMs have not only missed the trend towards electromobility, but, like VW with ID.3 for example, are now struggling with “manufacturing hell” themselves.

Is it just a fraud?

But probably the biggest difference between the two companies is the issue of fraud. Wirecard had apparently cheated investors and the public for many years. Many sales and especially money/cash holdings were fictitious.

When the missing 1.9 billion euros came to light, this was the deathblow for the company and left the new CEO Freis with no choice but to go into insolvency. Just how big the real hole in the balance sheet will ultimately remain to be seen, and many additional issues, including possible money laundering and illegal activities, are likely to occupy the public’s attention even further.

The opaque business model with transactions on numerous accounts in all destinations around the world is difficult to understand. Also the fact that Wirecard had made acquisitions for large amounts in the past, where it is still not clear who the seller and thus the beneficiary of the payments is, raises many questions.

At Tesla, on the other hand, there are aggressive announcements by the CEO, which are often not achieved, such as that full autonomy will be achieved by the end of 2019, but the general business model is without doubt no fake, because you see more and more Tesla driving everywhere on the roads and the worldwide charging stations are being expanded more and more.

The Frank-Thelen Indicator:

Both shares were hyped by stock market “expert” Frank Thelen. Tesla, just like Wirecard before.

Closing:

Is Tesla the new Wirecard? This question can certainly be answered with a clear no. Wirecard’s balance sheet scandal and the question whether there are no other illegal activities on a large scale obviously have no parallels to Tesla. Although Elon Musk likes to polarize the world, as co-founder of Paypal and now with his achievements at Tesla, SpaceX and The Boring Company he can show many successes, which do not only look good on paper. Wirecard’s successes were, as mentioned, often only air bookings and high expectations announced to the capital market without any real substance.

The question of investors whether one can not also lose money with the Tesla share is certainly another. There are many valid arguments that the high price of the Tesla share is not justified and one could also suffer price losses as an investor.

| A | Wirecard | Tesla | Parallel |

| short seller | High short interest with big profits | Highest short interest in the USA with massive losses | Yes |

| Polarizing CEO | CEO with big announcements and many lawsuits against critics | CEO also with big announcements but many milestones achieved | Partly |

| No profit | Profit was probably manipulated for years – company now insolvent | Years of burning a lot of cash – profit is slowly being achieved | Yes |

| Poor technology | Often disadvantages compared to high-end players in the market | Lack of processing but good software and leading in batteries | Partly |

| Valuation | Wirecard was strongly overvalued, especially in 2018, even if the figures had been real | share trades on valuations that otherwise only the best software companies can achieve, so the question remains whether this is justified | Yes |

| Competition | There were stronger competitors but the market offered many growth opportunities | A highly competitive market where other newcomers are already broke | Partly |

| Fraud | Much of the business was invented and did not exist | Solid business | No |