A guest article by Ralf Wischmann (STARCON CO. LTD)

Slowly but steadily, it is picking up speed, the trend towards cashless payments in Germany. A year ago, a rather wait-and-see to cautious attitude was reported, but now the dam seems to be broken and cashless payment and the technology behind it as well as central players have become an indispensable part of the reporting, not least after the advertising effective roll-out of two almost “legacy providers” of e-wallets in Germany. Often, however, no distinction is made between digital solutions (e.g. e-wallets) on the one hand and payment systems or networks on the other.

Often, however, no distinction is made between digital solutions (e.g. e-wallets) on the one hand and payment systems or networks on the other.

There is a big difference between rolling out an offer for cashless payments and being successful with it, as many startups in the field of payment were also able to experience in Germany. The topic “Merchant Aquiring” or “how do I manage as a Payment Service Provider that the merchant also offers the payment solution offered by me” (and of course the customer also uses or installs it) provides material for his own article.

Success Factors

A key to success, and this should come as no surprise, is not only the customer’s demand, but also the company’s own aquiring team, which by the way is not only a component of many banks but also of providers of payment options in Asia who originally started out as “merchants”.

The best possible “Merchant Experience” seems to be just as important as the often quoted User Experience and might be a reason for the fact that an acceptance also with smaller dealers with usually “small tickets” (e.g. in the food sector) is secured. It is quite possible that the success of e-wallets from suppliers with a dealer background is based on a retailer’s own experience and “understanding” the requirements.

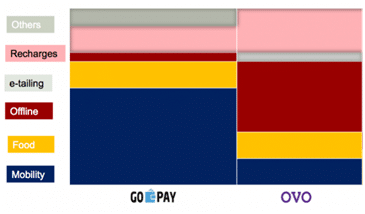

The distribution of the use of e-wallets between different points of acceptance of two providers that originally started in the mobile sector (Grab and Go-Jek) illustrates the role of an aquiring team.

E-Wallets central mobility provider and category split of deployment

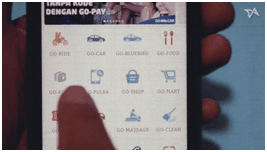

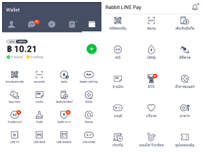

In addition to the two providers cited, a wealth of merchants and providers of digital communication platforms (such as Line) in Asia are now relying on their own payment / e-wallet solutions. At an early stage, they recognized the importance of payment as a central means of increasing customer satisfaction and loyalty and as a link / enabler for their own digital ecosystems and super apps, not least due to the supra-regional triumphal march of the two best-known providers from the Middle Kingdom, which is now also known in Europe.

SuperApp using Go Jek and Line as an example

https://nextunicorn.ventures/who-is-winning-in-the-battle-for-e-wallet-domination-in-southeast-asia/

Potential on the cost side by paying with an e-wallet from one’s own company at one’s own “POS” is not described on the press side, but cannot be ruled out, especially in the case of nationally active companies.

At one point or another, the scope is already being significantly expanded and the range of services offered by former classic retailers is being supplemented by further financial services in addition to payment. Most recently, for example, through a company that is also active in Germany via its own shareholdings.

How quickly a retailer’s own payment option becomes a central player and impressively wins the customer’s favour is impressively demonstrated by the development of the aforementioned provider with headquarters in Indonesia.

It remains to be seen whether locally dominant providers will also be able to assert themselves nationwide. However, the race for the customer’s favour has begun and the customer can (still) choose extensively from a wide range of e-wallets, be it from traditional financial service providers or other providers, increasingly from dealers.

“The race for the customer’s favour has begun.”

An option or vision also for Germany ?

The author

Ralf Wischmann, co-founder of STARCON CO LTD, a Bangkok-based company focusing on StartUp Advisory and Payment Innovation and driving cross-company initiatives in the area of C2B and B2B customer payment solutions at Deutsche Lufthansa AG until mid-2018.